Cash flow statement is one of the three key financial statements. It is prepared along with statements of profit & loss and balance sheet as it provides vital information about liquidity and the cash cycle of the business throughout the year.

Three Categories of Cash Flow Statement

Statement of cashflow provides information about cash utilized or generated from three key categories or areas of business i.e., operating activities, financing activities, and investing activities.

A statement of cash flow is used to present information in a way to reflect changes in an entity’s cash and cash equivalents during the accounting period.

Operating Activities: Operating activities are the principal revenue-producing activities of the business and other activities that are not included in investing or financing activities. These are the prime activities from which the entity generates its cash flows.

Some examples of cash generated and spent on operating activities are cash receipts for the sale of goods or services, cash receipts of other income, payment to suppliers, and payment for taxes.

Financing Activities: These are activities that result in changes in the size and composition of the contributions and borrowings of the business.

Some examples of cash generated and spent on financing activities are cash proceeds from issuing shares and debentures, cash proceeds from loans and borrowings, and cash payments of loans.

Investing Activities: These are the acquisition and disposal of long-term assets made by the business. These also includes other investments made by businesses.

Some examples of cash generated and spent on investing activities are cash payments to acquire property, plant, and equipment and cash receipts from sales of property, buildings, intangibles, and other long‑term assets.

Direct vs Indirect Cash Flow Method: What to Choose for Your Business?

While both methods serve the same purpose, they differ in how they report cash flows from operating activities. Choosing between the direct and indirect method for preparing the cash flow statement will depend on various factors like the accounting policy, size and complexity of the business, industry norms, and stakeholder preferences.

The direct method is more suitable for small to medium-sized businesses as the number of transactions is less and it’s easy to track cash transactions in detail. It is also suitable for businesses following the cash basis of accounting. But for large-scale businesses where there are hundreds of transactions going on daily, it’s better to opt for the indirect method of preparing a cash flow statement. The Indirect method is also recommended by IFRS(International Financial Reporting Standards) and GAAP(Generally Accepted Accounting Principles).

Direct Vs. Indirect Method of Cash Flows: Key Differences

The statement of cash flow can be prepared with either a direct method or an indirect method. Both methods are commonly used among different businesses, and they result in the same net cash balance at the end of the reporting period.

When choosing between the two methods, consider how cash is generated or spent on operating activities as the cash flow format for financing and investing activities remains the same.

| Direct Method | Indirect Method |

| It provides a detail of actual cash inflows and outflows from operations. It provides an actual picture of all major classes of gross cash receipts and gross cash payments. | It starts with net profit or loss of business and then non-cash transactions like depreciation are adjusted to reach net cash flows from operating activities. |

| More compatible with cash basis of accounting. | More compatible with the accrual basis of accounting. |

| Actual cash transactions for receipts and payments are used. | The effect of non-cash transactions is used in calculating net cash flows. |

| The direct method is acceptable under both IFRS and GAAP. | Both IFRS and GAAP encourage the use of the Indirect method. |

| No adjustment of non-cash transactions is required. | Net income is adjusted against non-cash transactions. |

Direct Cash Flow Statement

The direct method of preparing the cash flow statement involves adding all cash receipts and deducting all cash payments from operating activities. It is more based on the cash basis of accounting and provides a more detailed and straightforward view of cash movements in and out of a company’s operations.

It adds up all sales and deducts all costs to find out the net cash flow.

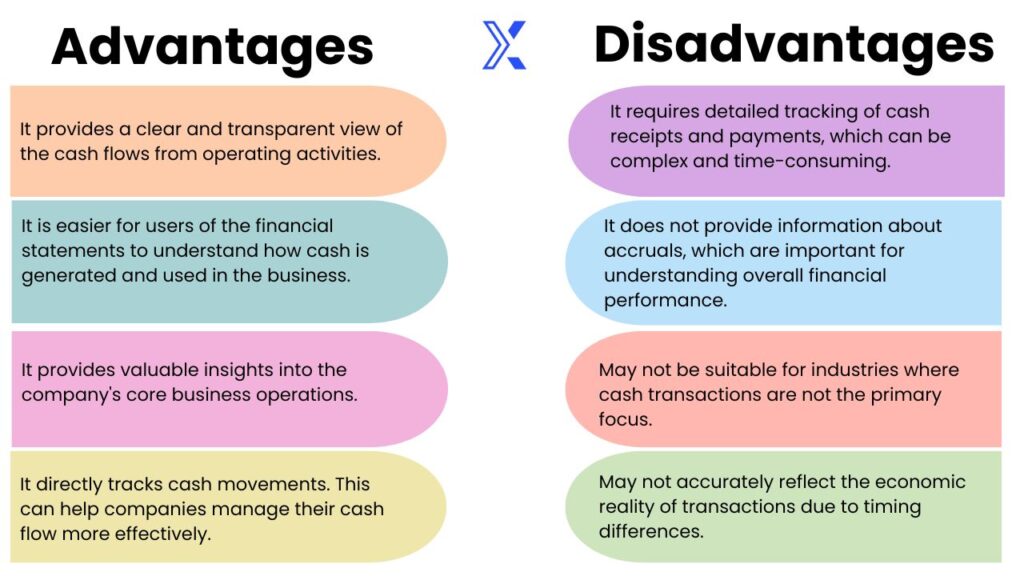

Advantages & Disadvantages of the Direct Method

Example of Direct Method Cash Flow Statement

The direct method of cash flow will add up gross cash receipts and take out cash expenses.

| Amount ($) | |

| Cash Sales | 400,000 |

| Other Income Received | 50,000 |

| Cash Paid- Suppliers | 200,000 |

| Cash Paid- Employees | 100,000 |

| Taxes Paid | 40,000 |

| Rent Income Received | 100,000 |

| Admin Expenses Paid | 35,000 |

The cash flow statement form direct method will be calculated as follows:

| Amount ($) | |

| Gross Cash Receipts: | |

| Cash Sales | 400,000 |

| Other Income Received | 50,000 |

| Rent Income Received | 100,000 |

| Total Cash Inflows | 550,000 |

| Gross Cash Payments: | |

| Admin Expenses Paid | 35,000 |

| Cash Paid- Suppliers | 200,000 |

| Cash Paid- Employees | 100,000 |

| Taxes Paid | 40,000 |

| Total Cash Outflows | (375,000) |

| Net Increase / Decrease In Cash Flows | 175,000 |

Note that, for simplicity this is only cash flow from operating activities.

Indirect Cash Flow Statement

It is called the indirect method because it indirectly calculates net cash flows from operating activities by starting with net income or loss for the reporting period.

The cash flow format for calculating cash flows from investing and financing activities remains the same for both direct and indirect methods, it just differs for cash flow from operating activities.

In the direct method, we don’t consider adjusting non-cash adjustments like depreciations and amortizations instead cash payments are deducted from cash receipts to reach net cash increase or decrease from operating activities.

The indirect method starts with net income or loss, taken from the income statement, and then noncash transactions like depreciation and working capital changes are adjusted to reach net cash flows from operations.

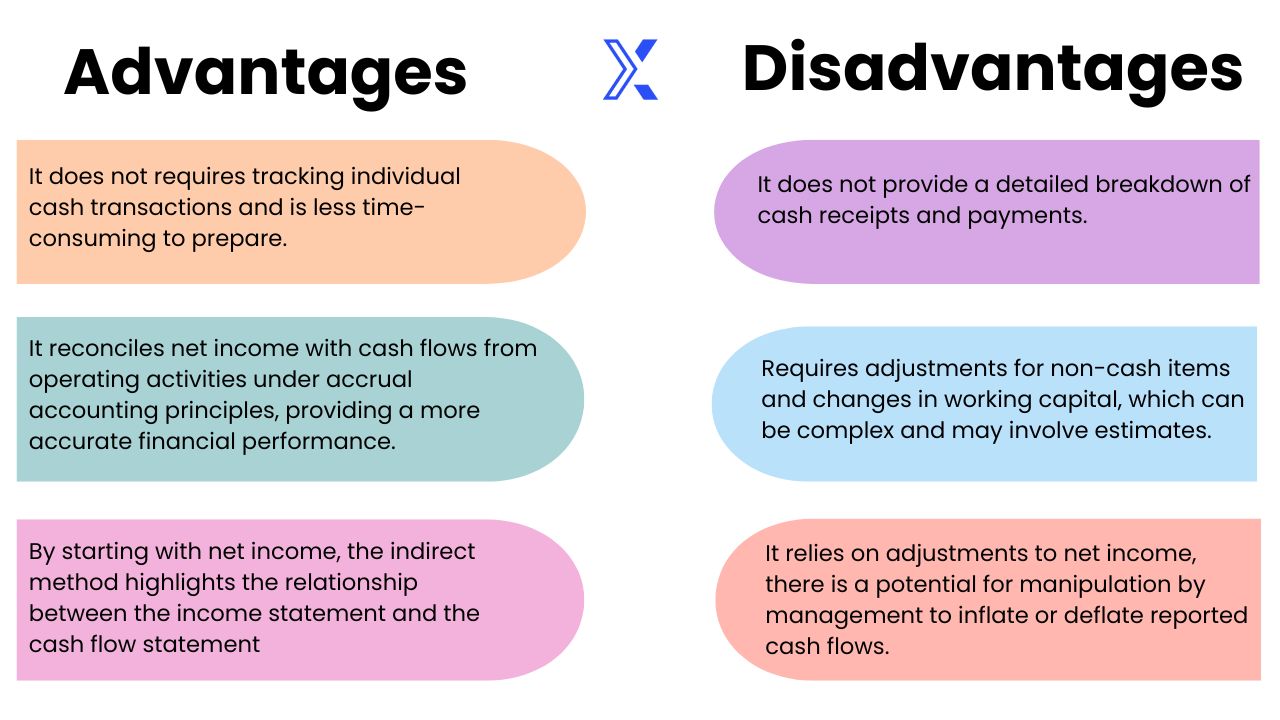

Advantages & Disadvantages of the Indirect Method

Example of Indirect Method Cash Flow Statement

The Indirect method of cash flow will add or less noncash adjustments and working capital changes to net income or loss to reach net cash flows from operating activities.

| Amount ($) | |

| Taxes Paid | 30,000 |

| Depreciation Expense | 25,000 |

| Increase in Accounts Receivable | 25,000 |

| Increase in Accounts Payable | 20,000 |

| Inventory Purchased | 35,000 |

| Net Income | 220,000 |

The cash flow statement form indirect method will be calculated as follows:

| Amount ($) | |

| Net Income | 220,000 |

| Adjustments: | |

| Add: Depreciation | 25,000 |

| Operating Profit | 245,000 |

| Working Capital Changes: | |

| Less: Increase in Accounts Receivable | (25,000) |

| Add: Increase in Accounts Payable | 20,000 |

| Less: Inventory Purchased | (35,000) |

| Cash Flow After Working Capital Changes | 205,000 |

| Less: Taxes Paid | (30,000) |

| Net Increase In Cash Flows From Operating Activities | 175,000 |

You can see how the cash flow from operating activities using the direct method and indirect method resulted in the same cash increase at the end with different adjustments.

Here is how noncash transactions and working capital adjustments result in an increase or decrease in cash flows:

Hi, I am Basit. One of guys behind XquisiteBooks. I have been in accountancy and finance profession since last 7 years and have worked in many organizations on different executive roles. Whether its bookkeeping, financial analysis, accounts receivable, accounts payable or working with general ledgers, I have served the finance industry and gained in-depth knowledge and exposure in my domain.

If you want to know more about me or our team, check out the about us page.