Cash flow management is crucial for the long-term sustainability and mission success of nonprofit organizations. The cash flow statement provides valuable insights about the cash inflows and outflows and plays a pivotal role in the financial and liquidity health of an organization.

A cash flow statement is a financial statement that provides an overview of the cash inflows and outflows of an organization over a specific period. It helps to analyze operating efficiency in terms of liquidity. It sub-categorizes these cash flows into operating activities, investing activities, and financing activities.

Statement of cash flows (CFS) complements the income statement and balance sheet and helps to provide valuable information to internal and external stakeholders about the entity’s ability to manage the cash flow cycle and run the operations.

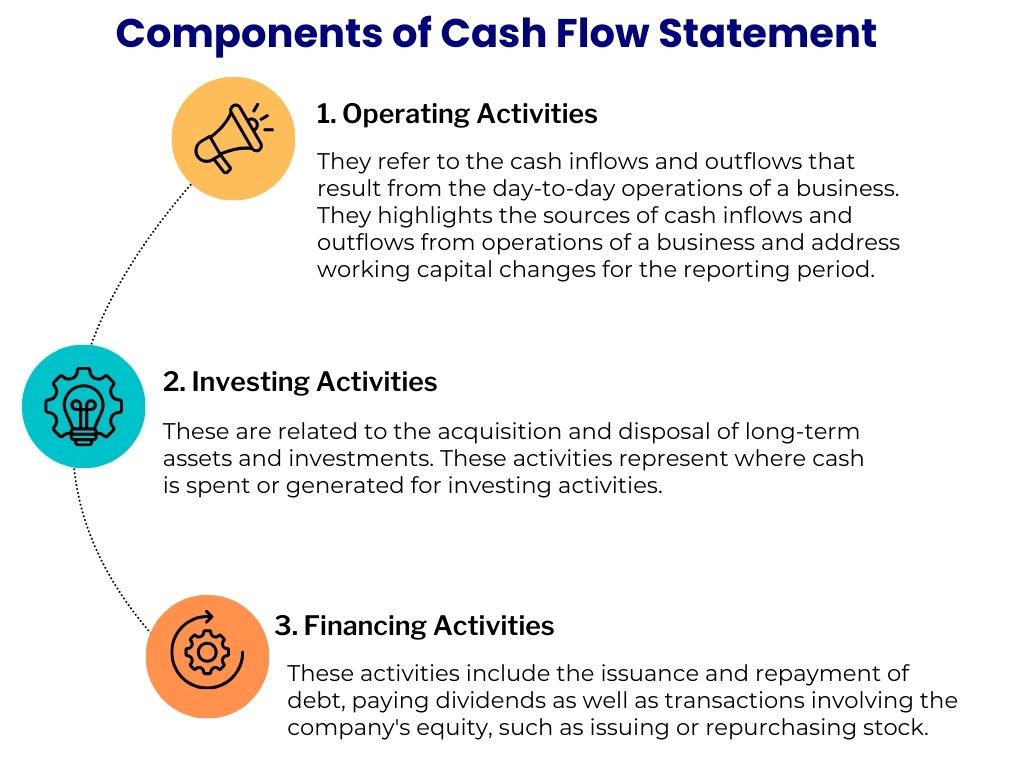

Categories of Cash Flow Statements

Operating Activities: Cash flow from operating activities gives an overview of the cash generated from main revenue-generating activities and cash used in day-to-day operating activities.

The main operating activities that generate cash flows for nonprofit organizations are donations, grants, program fees, and fundraising activities. And the operating activities for which cash is utilized are salaries, utilities, rent, and other day-to-day expenses.

Investing Activities: Cash flow from investing activities presents cash flows generated or used in the acquisition and disposal of long-term assets, such as property, equipment, and investments. This figure gives stakeholders an overview of how much the organization spends on property, plant, and equipment (PPE).

This section also provides details for cash flows from loans made to other organizations or investments in securities.

Financing Activities: Cash flow from financing activities presents net cash used to fund and manage an organization’s needs. Financing activities include net cash utilized or obtained from borrowing or repaying loans, changes in bank overdrafts or lines of credit, and cash payments for interest.

Cash Flow Statement Template

This cash flow statement template provides a format for creating cash flow statements using direct methods. You can record cash flows from operating, investing, and financing activities annually. Following this format, there is an Excel file template for a statement of cash flow.

Direct Vs. Indirect Method for Preparing Cash Flow Statement

Statement of cash flows can be prepared with direct and indirect method. Both methods serve as the basis for creating a cash flow statement and are helpful in providing insight into the net cash movements for a certain period.

Both methods are acceptable under GAAP in the US. Cash flow from financing and investing activities are calculated in the same manner under both of these methods but cash flow from operating activities are calculated differently.

The indirect method is more commonly used by medium and large-sized organizations. This method of preparing cash flows is suitable for organizations following an accrual basis of accounting.

The direct method focuses on cash inflows and outflows while providing only limited detail,

particularly of cash outflows.

The indirect method focuses on disclosing items that do not use or provide cash.

Direct Method

It is a straightforward method that uses actual figures to calculate net cash flows from payments and receipts.

Cash flow from operating activities is calculated by deducting payments made by the organization for rent, utilities, entertainment, salaries, supplies, and other operating expenses out of cash receipts from donations, fundraising, and other subscriptions.

The direct method provides a more detailed real-time view of cash flows from operating activities but requires more detailed information as well.

Indirect Method

The indirect method takes net income from the income statement and adjusts it against non-cash items and changes in working capital to arrive at cash flows from operating activities. Then cash flow from investing and financing activities are calculated to reach at closing cash balance for the period.

Common non-cash items used are depreciation, amortization, gain, or loss of disposal of assets.

Changes in working capital include increases or decreases in inventory, accounts receivable, accounts payable, and other current assets and liabilities appearing on the balance sheet of the entity.

Let’s create a statement of cash flow using both methods below.

Practical Steps: How to prepare cash flow statements for nonprofit organizations

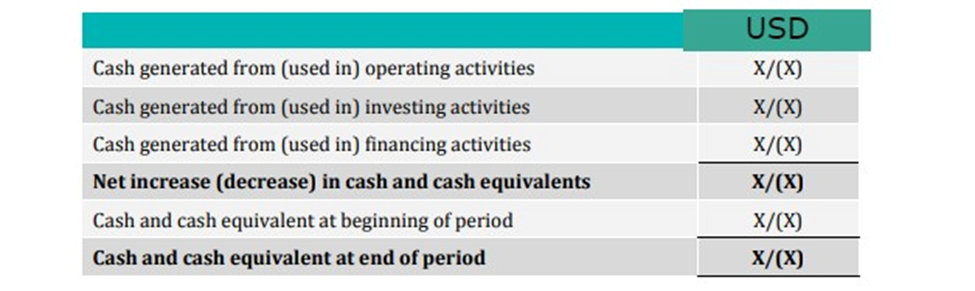

Let’s have a look at a simple summary of all cash flows calculated from operating, investing, and financing activities. After calculating the net cash flow from each of these three sections, the opening balance of cash and cash equivalents is added to reach the closing figure for net cash and cash equivalents at the end of the year.

While calculating cash flows from operating activities, we also have to account for changes in working capital. Working capital refers to the difference between current assets and current liabilities of the entity and is an important indicator of an entity’s ability to meet its short-term obligations.

The changes in working capital are represented in the statement of cash flows as:

Increase in assets: cash outflow

Decrease in assets: cash inflow

Increase in liabilities: cash inflow

Decrease in liabilities: cash outflow

Let’s take some sample data and create a statement of cash flows:

| Description | Amount ($) |

| Subscriptions | 280,000 |

| Grants | 490,000 |

| Consultancy receipts | 510,000 |

| Gross receipts | 1,280,000 |

| Operating expenses | (400,000) |

| Fund raising costs | (290,000) |

| Administrative expenses | (325,000) |

| Interest charges | (50,000) |

| Depreciation | (25,000) |

| Tax | (40,000) |

| Net Surplus | 150,000 |

Extracts from the statement of financial position:

As at 1 Jan 23 As at 31 Dec 23

| Inventory | 118,000 | 124,000 |

| Trade receivables | 233,000 | 219,000 |

| Trade payables | 102,000 | 125,000 |

| Accrued salaries | 8,000 | 5,000 |

| Accrued interest charges | 30,000 | 45,000 |

| Tax payable | 52,000 | 43,000 |

Other Information:

- Loan of USD 265,000 was taken this year.

- During the year plant which originally cost USD 69,000 was disposed of for USD 41,000.

- New equipment costing USD 56,000 was purchased during the year.

Statement of Cash Flow (Using Direct Method)

For the year ended 31 Dec 2023

Now, let’s prepare cash flow statement by indirect method:

| Amount ($) | |

| Cashflow from operating activities: | |

| Net surplus before tax | 190,000 |

| Adjustments: | |

| Depreciation expense | 25,000 |

| Interest expense | 50,000 |

| Working capital changes | |

| Inventories (124000-118000) | (6,000) |

| Trade payables (102000-125000) | 23,000 |

| Trade receivables (233000-219000) | 14,000 |

| Accrued salaries (8000-5000) | (3,000) |

| Cash generated from operations | 293,000 |

| Interest paid (50,000 + 30,000 – 45,000) | (35,000) |

| Income taxes paid (40,000 + 52,000 – 43,000) | (49,000) |

| Net cash inflow from (used in) operating activities | 209,000 |

| Cashflow from investing activities: | |

| Disposal proceeds of plant | 41,000 |

| Purchase of new equipment | (56,000) |

| Net cash outflow from (used in) investing activities | (15,000) |

| Cashflow from financing activities: | |

| New loan taken | 265,000 |

| Net cash inflow from (used in) financing activities | 265,000 |

| Net increase /(decrease) in cash and cash equivalents | 459,000 |

Now lets create cash flow statment using direct method:

Statement of Cash Flow (Using Direct Method)

For the year ended 31 Dec 2023

You see how the net cash and cash equivalents using both methods are the same.

The difference lies in the approach to calculating cash flows. By direct method, we have to start with gross receipts and then subtract cash payments. While using the indirect method, we start with net surplus/deficit for the period before taxes then adjust the non-cash transactions followed by working capital changes.

The Importance of the Cash Flow Statement for Nonprofits

The cash flow statement is a pivotal tool for financial management for nonprofit organizations for several reasons:

Cash Management: Cash management is critical for the survival of any organization and the same goes with nonprofit organizations. It helps nonprofits manage their cash resources effectively by dividing the cash generated and utilized in three sections: operating activities, financing activities, and investing activities. This allows organizations to know the areas for inflows and outflows of cash and identify areas for potential cash shortages or surpluses.

Financial Planning: By analyzing historical cash flow patterns, nonprofits can establish an understanding of areas of their spending which will help them to plan and optimize their cash flows in those areas.

By knowing the primary sources of inflows and outflows of cash it’s easy to plan for future expenses and revenue.

Decision Making: The cash flow statement helps in decision-making by providing insight into key cash resources of the organization. Cashflow is the key figure based upon which many decisions are taken. The more optimized the cash flow the better decisions can be taken. It is considered a key performance indicator for the long-term sustainability of any organization.

Some examples of decision-making for nonprofits can be whether to invest in new programs or projects, or whether to pursue additional fundraising efforts.

Accountability and Transparency: It provides transparency by tracking and monitoring the movement of cash within an organization, ensuring that funds are allocated appropriately and used efficiently.

Statement of cash flow also ensures accountability and helps businesses to mitigate financial risks and run operations efficiently.

Hi, I am Basit. One of guys behind XquisiteBooks. I have been in accountancy and finance profession since last 7 years and have worked in many organizations on different executive roles. Whether its bookkeeping, financial analysis, accounts receivable, accounts payable or working with general ledgers, I have served the finance industry and gained in-depth knowledge and exposure in my domain.

If you want to know more about me or our team, check out the about us page.